Tranalysis

[Editor's Note]

"Looking at Shanghai in Beijing" and the "Surging Afternoon Tea/Between Beijing and Shanghai" series of seminars were officially launched on May 17, 2024. "Between Beijing and Shanghai" aims to analyze central government policies and explore Shanghai's ideas.

the firstseminarWe invited historian Xiao Donglian, researcher Liu Yunzhong, researcher at the Development Strategy and Regional Economic Research Department of the Development Research Center of the State Council, Fan Shitao, associate professor at the Institute of Economics and Resource Management of Beijing Normal University, and Nan Chuxin, director of the Scientific Research Department of the China Economic System Reform Research Association, to talk about China's Shanghai strategy in its economic transformation.

From macro trends to specific issues. The second seminar focused on the construction of an international financial center and invited Yu Yongding, member of the Chinese Academy of Social Sciences, Pan Yingli, professor of Antai School of Economics and Management, Shanghai Jiao Tong University, Xu Mingqi, vice chairman of the Shanghai Center for International Economic Exchanges, and Director of the Institute of Financial Law of the Central University of Finance and Economics Huang Zhen, Zhang Tao, Financial Markets Department of China Construction Bank, Yang Panpan, Director of the International Finance Research Office of the Institute of World Economics and Politics, Chinese Academy of Social Sciences, Zhang Jianpeng, Deputy Director of the Policy and Regulation Department of the Shanghai City Local Financial Supervision Bureau, Wu Minchao, Director of the Cross-Border Finance Department of the Shanghai Pudong Development Bank Head Office, and Zhang Jun, Deputy General Manager of Lingang Group New Area Economic Company, were nine guests.

The seminar guests reached three consensuses: first, for the construction of an international financial center, Shanghai has the best conditions, but Shanghai alone is not enough and requires the joint efforts of the central and local governments; second, the construction of an international financial center must enhance the level of internationalization and be in line with international standards and rules; third, the pace of building an international financial center can be taken further.

The following are the highlights of Yu Yongding's speech. Yu Yongding talked about several views on the U.S. economy and the Chinese economy to provide background materials for discussions on the construction of Shanghai's international financial center.

Yu Yongding, a member of the Chinese Academy of Social Sciences, believes that to achieve China's economic growth target of 5% in 2024, the government needs to further issue additional treasury bonds, support infrastructure investment, support small and medium-sized enterprises and vulnerable groups, and support the resolution of financial risks. The Paper Journalist Zhou Pinglangtu

a

Whether a city can become an international financial center generally meets the following conditions:

· Bringing together a large number of financial talents and other professionals

· Not only have competitive regulations but also have high-quality law enforcers

· Preferential tax arrangements

· A government that responds to industry concerns

· A fair and fair business environment

· Good living environment (quality of life, culture and language)

· Easy access to international financial markets

· Reasonable operating costs, excellent commercial infrastructure

· High-quality commercial real estate

According to some questionnaires, the most important condition seems to be a good business environment.

Whether a city can become an international financial center, or whether the time is right to build a city into an international financial center, depends not only on the city's own conditions, but also inseparable from domestic and foreign economic and financial development and economic and financial situation. Shanghai is undoubtedly the city most qualified in China to become an international financial center. However, many of the necessary conditions for building Shanghai into an international financial center are beyond Shanghai's own decision. For example, capital account liberalization, free floating of the exchange rate (Hong Kong, as a city, may be pegged to the US dollar for a certain period of time), internationalization of the RMB, etc., all of which need to be decided by the central government and implemented nationwide.

Building Shanghai into an international financial center is a significant but very difficult undertaking. I will not specifically study this issue and have no say. I just want to make a few views on the U.S. economy and the Chinese economy here to provide some background materials for the discussion of the construction of Shanghai's international financial center.

second

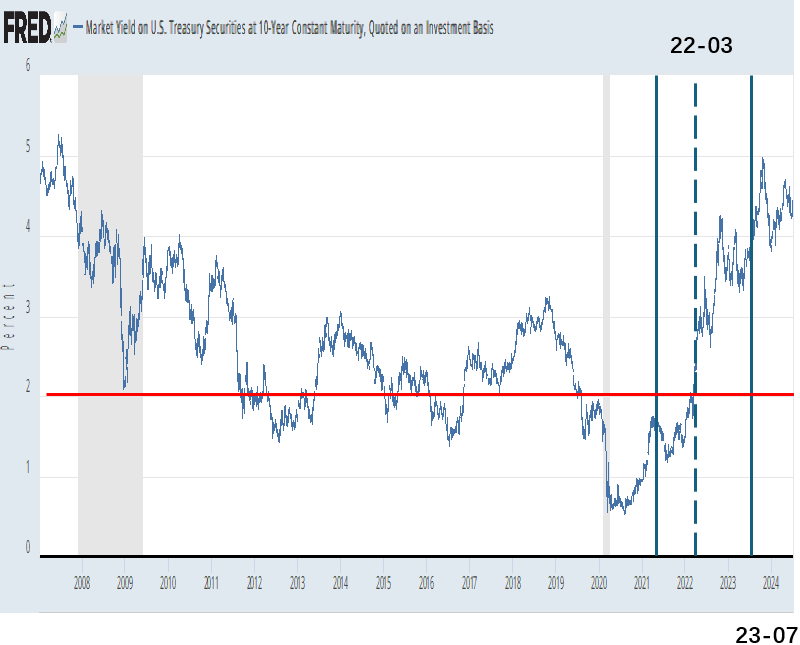

The evolution of the U.S. economy after the global financial crisis broke out in 2008 can be divided into many stages (Figure 1). These include several policy adjustments made by the U.S. government and the Federal Reserve from 2008 to March 2020. What I want to talk about today is the changes in the U.S. economy after March 2020.

Figure 1: Market yields on U.S. Treasury bonds Photo source: Federal Reserve

In March 2020, against the background of the epidemic outbreak and supply chain disruption, the U.S. stock market suddenly plummeted for various reasons. From February 12, 2020 to March 20, 2020, the Dow Jones stock index plunged 35.1%, and US dollar liquidity dried up. In order to rescue the market, on March 23, the Federal Reserve announced an unprecedented "bottom-line" rescue plan and launched an unlimited quantitative easing model. At the same time, the Federal Reserve also resumed its zero-interest-rate policy. Since then, in just three months, the Federal Reserve's balance sheet has soared from about US$4 trillion to more than US$8 trillion, reaching a peak of US$8.9 trillion.

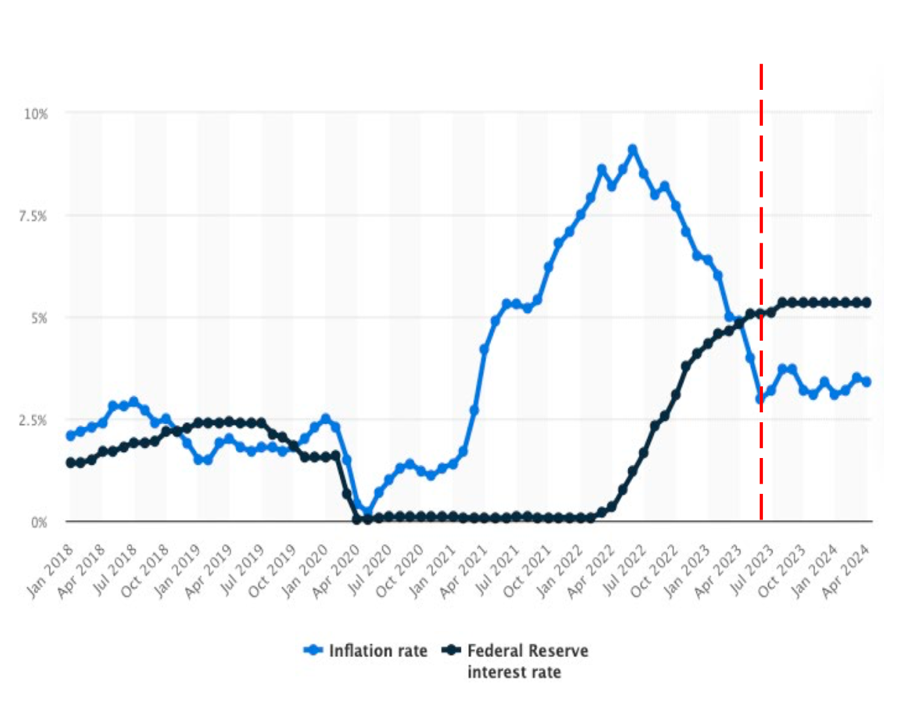

In March 2021, inflation exceeded the 2% target and began to rise.There are basically two reasons for inflation in the United States: first, external shocks. In particular, the COVID-19 epidemic caused supply chain interruptions, trade frictions with China and other things, and the total supply curve shifted to the left. Second, in order to support the stock market, the Federal Reserve adopted an extremely expansionary monetary policy, and the U.S. government implemented an extremely expansionary fiscal policy in response to the impact of the COVID-19.

The Federal Reserve's mistake is that after inflation exceeded 2%(2.6%) in March 2021, it only emphasized the role of supply shocks, while ignoring the increase in consumption and investment, especially household consumption demand, on prices after March 2020. The lifting effect. Since the subprime mortgage crisis in 2008, although the Federal Reserve has been implementing expansionary monetary policy, the inflation rate has remained at around 2% except in 2013. After March 2020, the situation finally changed. Ultra-expansionary fiscal money finally led to a sharp rise in inflation. At the same time, the U.S. fiscal deficit reached a staggering 14.9% and 10% of GDP in 2020 and 2021 respectively.

The experience of the United States shows that although extremely loose monetary policy may not lead to inflation for a long time. But in any case there should be a threshold, and once crossed, inflation could suddenly deteriorate.China's quasi-deflationary state provides us with a window to implement expansionary fiscal and monetary policies. If we do not actively seize the time to stimulate economic growth through expansionary fiscal and monetary policies and reverse the year-on-year decline in GDP growth since 2010, the window of opportunity may close at any time.

Figure 2: The Federal Reserve will raise interest rates 7 times in 2022 and 4 times in 2023, totaling 11 times. The target range for the federal funds interest rate increased from 0-0.25% at the beginning of 2022 to 5.25%- 5.5% in July 2023. There has been no interest rate hikes until now, but there has been no interest rate cut either. Except for special instructions, the charts in this article are all from Yu Yongding's speech PPT

Since the Fed believes that inflation is mainly caused by supply shocks, monetary policy is basically powerless to deal with inflation caused by supply shocks. At the same time, since the employment problem is still relatively serious, it is naturally unwilling to raise interest rates to curb inflation. The Fed's attitude will not begin to change until November 2021. In fact, the inflation rate in the United States in 2021 has reached 7%. The Federal Reserve will start raising interest rates in March 2022. Added 7 times in 2022 and 4 times in 2023. As the Federal Reserve raised interest rates, the U.S. inflation rate also began to gradually decline. It has dropped month by month from 9.01% in June 2022 (the highest record in 40 years) to 3.2% in July 2023. But since then, the Federal Reserve has not raised interest rates again, and inflation has basically remained at around 3%. The Federal Reserve's battle to curb inflation has entered a stalemate.

three

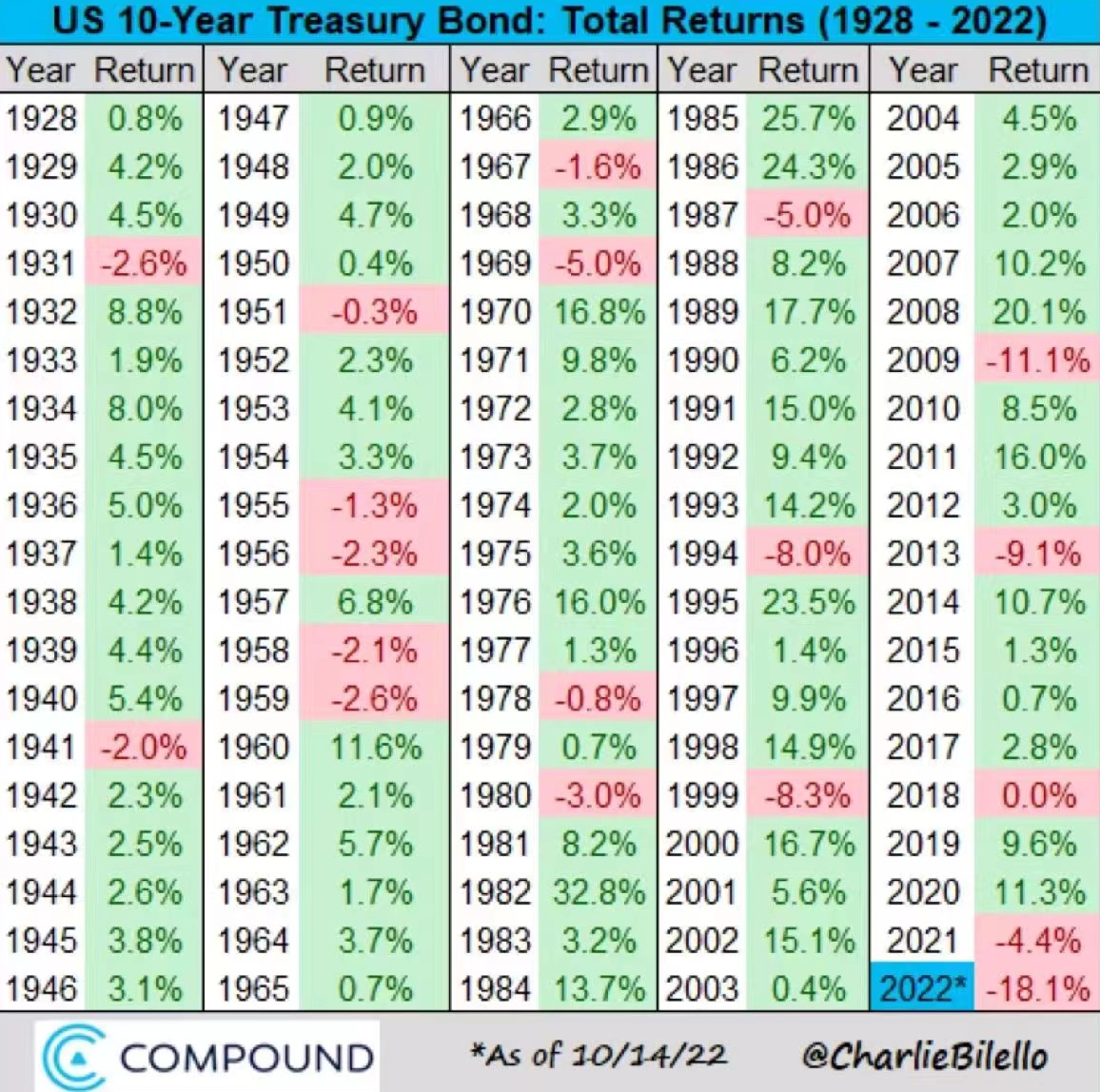

Figure 3: The return on U.S. 10-year Treasury bonds in 2022 is terrible

The Federal Reserve's interest rate hike has led to an increase in the yield curve of U.S. financial products. In October 2023, the yield on U.S. 10-year Treasury bonds was once close to 5%(4.98% on October 19). A rise in Treasury yields means a fall in Treasury prices. Just as falling house prices and falling stock prices cost holders of homes and stocks, holders of Treasury bonds and other fixed-income assets suffer heavy losses. Market participants exclaimed: "Impossible things" happened in 2022! As the "largest, deepest, most liquid, and risk-free" asset in the world, U.S. Treasury bonds actually achieved double-digit negative returns (Figure 3). After October 2023, the yield on the U.S. 10-year Treasury bond will start to decline. The phenomenon that the market is most concerned about in 2023 is the continued rise in U.S. Treasury yields. On October 19, 2023, the 10-year U.S. Treasury bond almost exceeded 5%.

Have U.S. fixed-income bond yields peaked or prices of fixed-income bonds bottomed out? The influx of giants such as Berkeley into the bond market shows that a turning point has arrived in their judgment of the U.S. economy, U.S. debt and the Federal Reserve's policies. But most investors are still waiting and see out of caution. In December 2023, as the Federal Reserve once again decided not to raise interest rates, more and more American investors made optimistic judgments about the U.S. economic situation (the inflation situation improved), and the U.S. 10-year Treasury bond yield began to fall. It was 3.88% at the beginning of 2023 and 3.88% at the end of the year. However, it will rebound to around 4.45% in July 2024.

The pattern of capital inflows in the United States has changed. In the past, foreign central banks bought treasury bonds and changed to private investors buying stocks around 2023. Global stock markets have soared in 23 years (except for the MSCI China Index and the Hang Seng Index). Semiconductors (SOX index) rose 64.90%, the Nasdaq 100 index (NDX index) rose 53.81%, and the Nasdaq Composite index rose 43.42%. Global stocks will perform well in 2023: Semiconductor: +64.90%, Nasdaq 100:+53.81%, Nasdaq Composite: +43.42%, Nikkei 225:+28.24%

The Federal Reserve's continued interest rates and rising U.S. Treasury yields have led to an influx of overseas funds into the United States. For the United States, the influx of overseas funds helps maintain the United States 'balance of payments and promotes a stronger dollar. The United States has maintained a current-account deficit for decades. Net overseas debt as a proportion of GDP is very high. The United States has long relied on foreign investors, especially foreign central banks and the Organization of the Petroleum Exporting Countries, to purchase U.S. Treasury bonds to maintain its balance of payments. Rising Treasury yields mean that the United States will have to pay a higher price to attract foreign investment.The Fed's maintenance of high interest rates means a steady inflow of overseas funds, and it also means that the United States 'net international investment position (NIIP) will accelerate its deterioration.

four

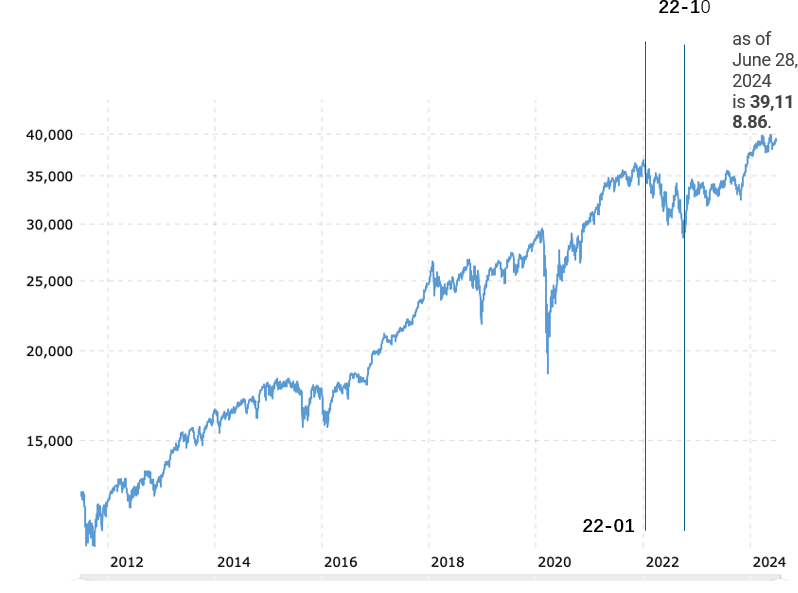

Figure 4: Dow Jones Index Trajectory: It performed poorly in 2022, but improved after October

The U.S. stock market performed poorly for a while in 2022, but improved after October. The performance between the two straight lines (Figure 4) was not very good, but later it went up again. Now it is almost over 40,000. Stocks performed well, the United States 'own funds withdrew, and private investors from other countries also bought in large quantities. The Dow has been rising. There are no particularly obvious signs of change yet.The United States will certainly benefit from the inflow of overseas funds into the stock market, but the inflow of stock market funds rather than government bonds into the United States and the appreciation of the US dollar will both lead to an increase in the net overseas debt of the United States.

In 2023, the net overseas debt of the United States will be US$19.58 trillion, reaching 80% of GDP. If it were a developing country, such as Mexico, a net overseas debt to GDP ratio of 40%, it would mean the outbreak of the "tequila crisis." In Southeast Asian countries such as Thailand, when net overseas debt to GDP was much lower than that of U.S. debt, a balance of payments crisis occurred. The currency depreciated sharply, and a large number of domestic companies went bankrupt due to the burden of foreign debt. However, the above-mentioned crisis did not occur in the United States because the US dollar still enjoys a high degree of credit for a long time, and the US dollar is almost the only international reserve currency. Foreign residents are still willing to hold US dollar assets. However, there is a limit to everything. It is impossible for overseas investors to never consider the continued increase in the ratio of U.S. overseas debt to GDP.

At some point in the future, we may face the crisis before 2008 again. The three major international credit rating agencies have successively downgraded the U.S. sovereign credit rating.If the U.S. net overseas debt-to-GDP ratio continues to rise, a so-called "sudden stop" is not impossible.

Since July 2023, although the market has been expecting the Federal Reserve to cut interest rates. The Federal Reserve has been inactive. The inflation rate has not changed much either. I have always believed that the main problem for the Fed is that it still adheres to the 2% inflation target set more than 20 years ago. Due to factors such as anti-globalization, the Russia-Ukraine War, and the US-China trade war, global supply chains have been severely damaged. In other words, the aggregate supply curve has shifted permanently to the left. Under such circumstances, if the Federal Reserve insists on reducing the inflation rate to 2%, the probability of stagflation in the United States will be greatly increased. If the Federal Reserve abandons its 2% inflation target and starts to cut interest rates, the credibility of the Federal Reserve's policies will be greatly reduced, and inflation expectations will no longer be anchored at a given level. This situation will cause great difficulties in the implementation of the Federal Reserve's future monetary policy. Not only that, but whether the American public can accept higher inflation is also a question. A convenient "solution" for the Fed is to pay lip service to the 2% inflation target, but not clear when it will be achieved, delay it indefinitely, and then act accordingly. The Fed does seem to be doing this right now.

five

Figure 5: High fluctuations in the US dollar index

Everyone cares about the RMB exchange rate and the changes in the US dollar. Figure 5 plots the trajectory of the dollar. The reasons are very complex. You can't simply explain it by using the Federal Reserve's interest rate hikes. Looking back now, China intervened in external markets on a large scale from 2015 to 2016 to stabilize the RMB exchange rate. In fact, whether the RMB appreciates or devalues is largely related to the external environment and a series of U.S. policies. From the end of 2016 to the beginning of 2017, the RMB stopped devaluing and stabilized. I don't think it was the result of intervention, but that the US dollar index stopped rising. Trump came to power, believing that the dollar was too strong and not conducive to exports, so the dollar would devalue. At that time, the exchange rates of all developing countries were stable.

So far, the exchange rate of RMB against the US dollar is 7.3. I still tend to wait and see and not intervene too much, especially because of the stability of the exchange rate, which will not change my stance on implementing expansionary monetary policy and expansionary fiscal policy.

We do face the possibility that the RMB may depreciate further. At this time, we need to make choices. We should not attach too much importance to stabilizing the exchange rate now. Exchange rate devaluation is a "double-edged sword" that has advantages and disadvantages. We are concerned that expectations of devaluation will accelerate capital flight.Judging from the figures provided by the Bank of New York Mellon, the peak of China's capital outflow has passed, and everything that should have escaped has escaped. In fact, many foreign investment banks are now preparing to re-enter China.

six

First of all, we need to make it clear that at the macroeconomic level, China's current problem is insufficient aggregate demand or effective demand.Second, we know that aggregate demand can be divided into three major blocks: final consumption, capital formation, and net exports. Third, based on known data, it can be assumed that the proportions of these three blocks in GDP at the end of 2023 will be 54.7%, 42.8% and 2.5% respectively. Therefore, in terms of economic growth in 2024, the normative question is: What will final consumption, capital formation and net exports each contribute to the 5% GDP growth target? In fact, in 2023, among the 5.2% GDP growth rate, consumption, investment and net exports contributed 4.3 percentage points, 1.5 percentage points, and-0.6 percentage points, and their contribution rates to economic growth were 82.5%, 28.9%,-11.4% respectively. Obviously, consumption will contribute the most to GDP growth in 2023.

The year-on-year growth rates of consumption (social zero), investment (fixed investment) and net exports from January to May 2024 were 4.1%, 4.0% and 3.2% respectively, and their contributions to GDP growth were 2.24 percentage points, 1.7 percentage points and 0.13 percentage points respectively. Apparently,So far, consumption remains the main driver of GDP growth in 2024. Due to the basic disappearance of the base effect, the contribution of consumption to GDP growth has dropped significantly compared with 2023. The contribution of investment and trade surpluses to GDP growth will increase in 2024, but it is not enough to offset the negative impact of declining consumption growth on achieving the 5% target of GDP growth.1-5 Monthly manufacturing investment increased by 9.6% year-on-year, becoming the biggest highlight of China's economy in 2024. butThe growth rate of real estate development investment has dropped from nearly half of minus 9.6% in 2023 to 10.1%, which has seriously dragged down the growth of investment and in turn dragged down GDP growth.It could have been hoped that the significant increase in infrastructure investment growth would hedge the adverse impact of negative growth in real estate investment and declining consumption growth on GDP. However, from January to June 2024, national fixed asset investment increased by 3.9% year-on-year, and infrastructure investment (excluding electricity, heat, gas and water production and supply industries) increased by 5.4% year-on-year. Obviously, the growth rates of the two are far from enough to compensate for the impact of declining consumption growth on achieving the 5% growth target. Therefore, in the second half of 2024, the Chinese government must adopt more intensive expansionary fiscal and monetary policies, otherwise it will have no choice but to accept a lower GDP growth rate.

Due to the emergence of the "three new pieces" and other factors, manufacturing investment increased by 9.6% year-on-year from January to May 2024. The significant increase in manufacturing investment growth has partially offset the drag on fixed asset investment growth caused by a 10.1% year-on-year decline in real estate investment. But even so,The growth rate of fixed asset investment is far from enough to offset the adverse impact of declining consumption growth on GDP growth. Statistics show that I am afraid that only by significantly increasing the growth rate of infrastructure investment will China be able to achieve the 5% GDP growth target in 2024.

I personally believe that in order to achieve the 5% GDP growth target in 2024, China must increase the expansion of fiscal policies.In 2024, the government will issue 4.06 trillion yuan in general treasury bonds, 3.9 trillion yuan in special bonds, and 1 trillion yuan in ultra-long-term special treasury bonds, totaling 8.96 trillion yuan. The broad fiscal deficit reached 11.1 trillion yuan. Although the expansion of China's fiscal policy in 2024 will significantly exceed that in 2023, judging from the current situation, the central government should increase fiscal expenditures and support infrastructure investment further significantly.

Since 2024, China's medium and long-term bond yields have been declining. The 10-year Treasury bond yield remained roughly low at 2.21%, the 30-year Treasury bond yield fell below 2.5%, and the Treasury bond yield curve moved downward as a whole. Market participants believe that a large amount of bank deposits enter the bond market and long-term government bond yields are too low, which poses certain risks. I think that the issuance of various long-term treasury bonds has been smooth. The low level of treasury bond yields, especially long-term and ultra-long-term treasury bond yields, is certainly a response to the bank's "asset shortage", but it still more reflects investors 'confidence in China's economic prospects. Low bond yields indicate that the Chinese government still has room to further increase fiscal policy expansion. There is no need for the Chinese government to abide by the so-called Mastrich Treaty fiscal rules of "fiscal deficit ratio of 3% and national debt to GDP ratio of 60%." China also does not need to deny that the central bank buys new treasury bonds in the secondary market when necessary. China's main macroeconomic policy goal in 2024 is to achieve a GDP growth target of around 5%. "The opportunity is never lost, and the opportunity will never come again."China's current low inflation level allows us to confidently implement expansionary fiscal policies bolstered by loose monetary policies.Once inflation suddenly rises due to some kind of shock, we may be placed in a dilemma. We should have greater courage and determination to implement the central government's various economic work policies with the spirit of seizing the day, and firmly implement expansionary fiscal and monetary policies. Only in this way can China get out of the "L-shaped growth" dilemma that has been in place for more than 10 years.